When life throws an unexpected curveball, the financial impact can be overwhelming. A sudden car repair, an unexpected bill, or the cost of replacing a broken fridge often comes without any warning. For many New Zealanders, covering these essential costs means turning to high-interest credit cards, loans, or ‘buy now, pay later’ schemes – debt that can take months or years to pay off. This is where your safety net comes in: the emergency fund.

What is an Emergency Fund?

An emergency fund (also called a rainy day fund) is money you’ve set aside for life’s true surprises. It doesn’t need to be a huge amount to start – in fact, setting a small, achievable savings goal is the most powerful first step you can take.

This cushion gives you immediate peace of mind, reduces stress, and helps you handle the unexpected without derailing your long-term goals or taking on debt.

Why Do You Need an Emergency Fund?

- Avoid High-Interest Debt: Instead of relying on expensive loans or credit cards when emergencies happen, you use your own money. This helps you avoid the cycle of interest and fees that keeps you stuck.

- Peace of Mind: Knowing you have money tucked away acts as a buffer between you and financial worries. This reduces the stress of unexpected bills and gives you space to make better decisions.

- Stay in Control: Even a small fund gives you breathing room to handle surprises (like reduced work hours or an essential repair) without throwing off your regular budget or sacrificing your bigger goals.

Steps to Create Your First Emergency Fund

Building this fund is a journey of small, deliberate actions. Follow these six steps to reach your initial goal:

1. Set Your Laser-Focused Goal

Instead of feeling overwhelmed by saving three or six months of expenses (a goal that can come later), focus on an initial target that seems realistic to you. This amount should be enough to cover, or at least provide a buffer, for common emergencies such as your insurance excess, a car tow, or a new essential appliance.

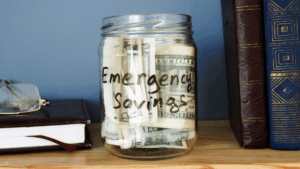

2. Open a Separate, Dedicated Savings Account

- The ‘Lockbox’ Rule: Open a separate savings account – ideally with a different bank or one that requires an extra step to access.

- Name It: Call it something clear, like “Emergency Savings” or “Rainy Day Fund.” This creates a mental reminder not to dip into it for non-emergencies.

3. Review Your Spending to Find the Money

- Identify ‘Budget Leaks’: Look for smaller costs or weekly expenses you could temporarily reduce. Could you cut back on takeaways to once a week? Cancel unused streaming subscriptions? Switch to a cheaper phone plan? You’ll be surprised at what a huge difference this makes.

- Calculate What You Can Save: Add up the changes you’ve made to see how much you can put aside each week or month. Those small cuts to everyday spending can really add up! Once you know your amount, you can figure out when you’ll reach your goal.

Here’s what your emergency savings could look like:

- Save $20 a week = reach $1,000 in one year

- Save $15 a week = reach $750 in one year

- Save $10 a week = reach $500 in one year

4. Start Consistent, Automatic Saving

- Pay Yourself First: Set up an automatic transfer from your everyday account to your emergency fund on payday. Treat this like any other bill you have to pay.

- Focus on the Habit: Saving consistently matters more than the amount. Once the habit sticks, you can always increase it later to get to your goal faster.

5. Boost Your Fund With Unexpected Income

Any money that comes your way outside your regular pay should go straight into your emergency fund, unless it is being used to cover existing debt. This speeds up your progress significantly. This might be tax refunds, birthday money, or even selling things you don’t use anymore – these are all great ways to boost your savings progress.

6. Acknowledge and Celebrate Your Milestones

Building savings is a marathon, not a sprint, so pause regularly to appreciate how far you’ve come – you should be proud that you’re taking the steps now to build these habits and provide a financial safety net for your future.

Emergency Fund FAQs

If I Have Debt – Should I Tackle That First?

If high-interest debt is holding you back, our interest-free loans (up to $5,000) can help you pay it off with zero interest and up to two years to repay. This frees you from those interest charges, while you can make small payments toward your emergency fund at the same time – covering all bases. You’ll also work with one of our supportive financial mentors, who will help you create a plan.

What If I Can’t Save Right Now?

If you’ve looked at your budget and there’s truly nothing to cut, you’re not failing – you’re dealing with a tough reality that many New Zealanders are currently experiencing. Start by saving whatever you can, even $2-5 a week, as these small amounts help to build the habit. When your circumstances change, it will be much easier to continue with this progress.

What If I Have an Emergency Before I Reach My Goal?

Even $200-300 saved is better than nothing. It might not cover everything, but it reduces how much you need to borrow.

You might save $300, then need to use $200 for an urgent bill. That’s okay – you’re still $100 ahead of where you started. Once you’ve handled the emergency, start saving again. Your emergency fund is working exactly as intended when you use it for a real emergency.

Building Your Money Confidence

Starting an emergency fund isn’t just about money – it’s about reducing financial stress, building confidence and taking control of your future. Even small, steady steps forward help reduce stress and give you the breathing room to handle unexpected expenses without falling back into debt.

The habits you’re building now – setting aside money regularly, making thoughtful spending choices, and prioritising your financial security – are skills that will serve you for life.

Get Support on Your Journey

You don’t have to figure this out alone. At Ngā Tāngata Microfinance, we’re here to help you build confidence and get ahead with your money.

If you need extra support with managing money, reducing debt, or learning to save smarter, My Money Kete is a free toolkit with practical workshops, access to interest-free loans and resources to help you reach your financial goals.

Ready to take the next step? Sign up today – we’re here to support you every step of the way.